Commercial Property GST Rate

The Complete GST Rules & Rates on Commercial Property in India for the Master Guide.

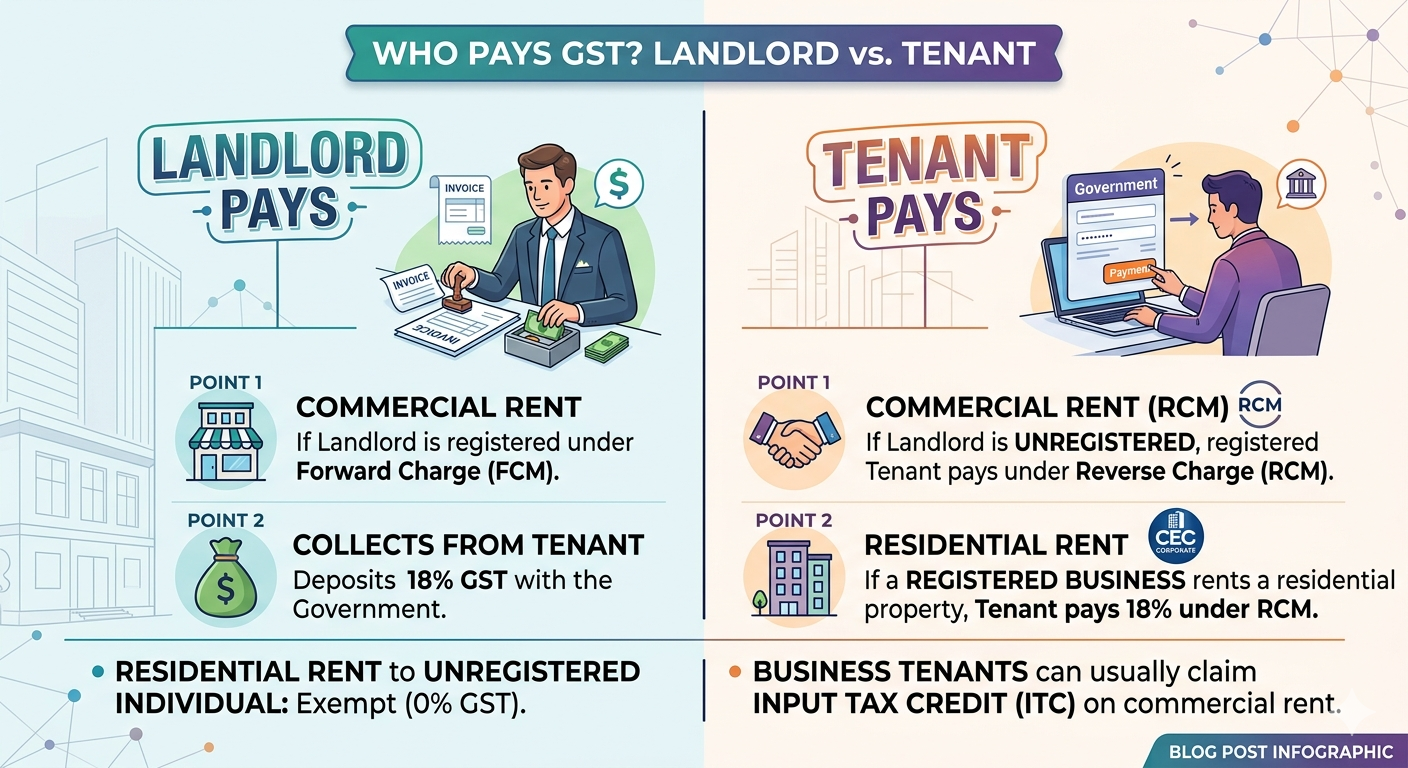

Who pays GST, landlord or tenant? A : GST is ultimately borne by the tenant, although who pays and how depends on the nature of lease and whether or not the owner is registered for tax.

Residential Properties

Personal Residence: if a person rents a home or apartment that the person occupies solely as a residence, there is no GST payable (even though the landlord may be registered).

Business Use: In case, a registered business entity or proprietor has rented any residential dwelling for commercial use or as an accommodation for his employees, the tenant shall pay GST (by way of RCM) directly to government.

Commercial Properties (Offices, Shops, Warehouses)

Standard Mechanism: Applicable 18% GST on commercial properties. The tenant is required to pay this GST every month with their rental payment to the landlord, and then subsequently remitted it (the funds are deposited by the landlord with tax authorities).

When a commercial space owner who is not registered under GST rents the premises to someone who is, it attracts 18% GST. In this case, reverse charge applies and the tenant pays this amount straight to the government.

In most cases of commercial establishments, the GST paid can be offset (as there are registered tenants who can claim an Input Tax Credit(ITC) suggestive obviously when the GST is being applied)

The payment of 18 % GST on rent either by landlord or tenant completely depends upon the nature of house property (commercial vs residential) and GST registration status of both parties.

The rules specify who exactly is liable to pay the tax in each situation:

Commercial Property (Shops, Offices, Warehouses)

Responsibility of commercial property is based under; FCM or RCM

Scenario A: Landlord is GST-Registered → Rent Paid by Landlord (FCM)

The landlord charges 18% GST on the rent bill, recovers from the tenant and pays it to Govt.

Case B: Unregistered Landlord + Registered Tenant $\rightarrow$Tenant Pays (RCM)

Especially after some important tax changes if a GST-registered business rents out commercial space from an unregistered landlord, then the tenant is compelled to calculate and pay the 18% GST directly to the government under RCM. There is no tax collected by the landlord.

Scenario C: Both Unregistered $\rightarrow No GST$

Where neither the landlord nor the tenant is liable to register under GST, rent pays no tax.

Residential Property (Flats, Houses)

Residential real property tax is calculated according to the usage of the property and by profiles of tenants.

Example A: Rented to a Non-Registered Person as Non-Residence $o$ No GST (Exempt)

If an undeclared individual or a salaried worker rents a home simply to live in, it is entirely free. Neither party pays GST.

Scenario B: Rented to a GST Registered Business $\rightarrow$ Tenant is Paying (RCM)

A registered company or firm that leases out a property for residential (like guest house, staff transit facility, home office etc.) use is also liable to pay tax @ 18% as applicable. This is to be paid directly to the government by the tenant business under RCM.

Scenario C: Leased to a Registered Owner for Occasional Use $\rightarrow$ No GST (Out of scope)

A registered sole proprietor who rents a home to live in with their family as such will also not have that deemed rental income subject to tax as long it is not claimed as an expense of the business.

| Property Type | Landlord Status | Tenant Status | Who Pays the 18% GST? | Can Tenant Claim Input Tax Credit (ITC)? |

|---|---|---|---|---|

| Commercial | Registered | Any Tenant | Landlord (via regular invoice) | Yes (if tenant is registered for business) |

| Commercial | Unregistered | Registered | Tenant (via RCM) | Yes (revenue-neutral for the business) |

| Commercial | Unregistered | Unregistered | No GST | N/A |

| Residential | Any Status | Unregistered | No GST (Exempt) | N/A |

| Residential | Any Status | Registered | Tenant (via RCM) | Generally No (blocked for personal use) |

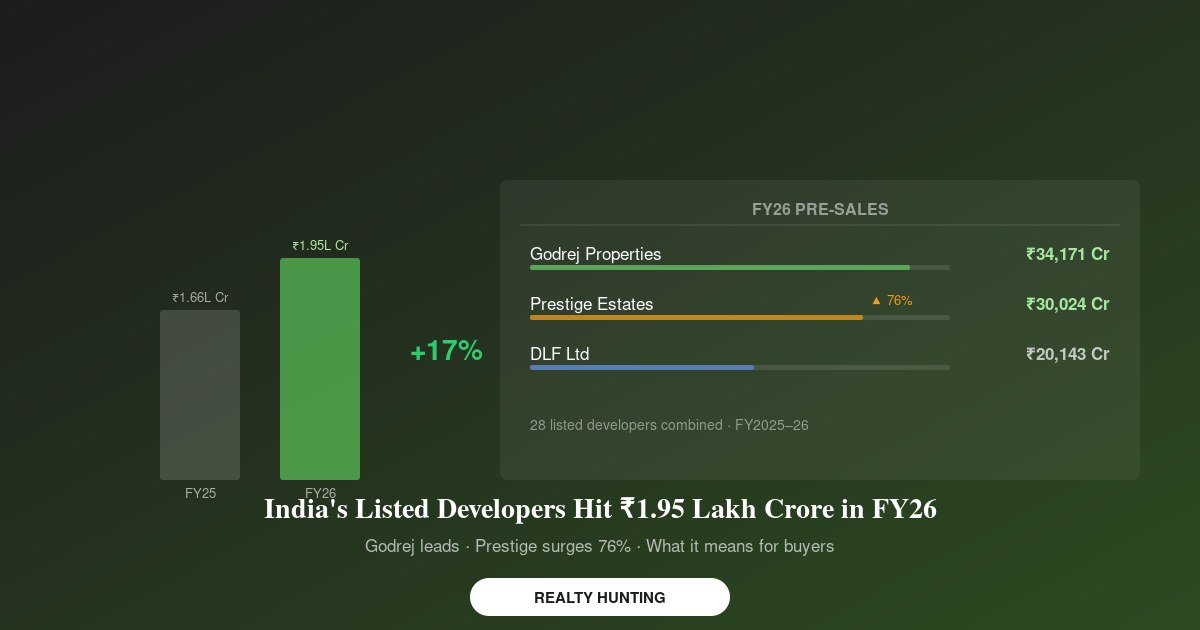

28 listed real estate companies clocked ₹1.95 lakh crore in pre-sales for FY26 — up 17% over FY...

Read more →

Prestige City Indirapuram Phase 1 sold ₹8,000+ crore of flats. Now the Mayflower phase (₹2,200...

Read more →

Noida averages ₹11,750/sqft and Greater Noida ₹8,100/sqft — but the gap isn't the only thing th...

Read more →If work is what brought you here, we can sort you a good office — ready to move or pre-rented, with parking, power backup and a proper address. Tell us your team size and budget and we will share the right options.

Share your number — we will call with the right options. No spam.

Or chat on WhatsApp Delivered

Delivered

Delivered

Delivered

Gurgaon.

Office Space

Rent / Lease

Rent / Lease

Coming Soon

Coming Soon

Sector 113 Gurgaon

Office Space

Get the latest price, layout and a site visit for any project in Gurgaon & Delhi-NCR.