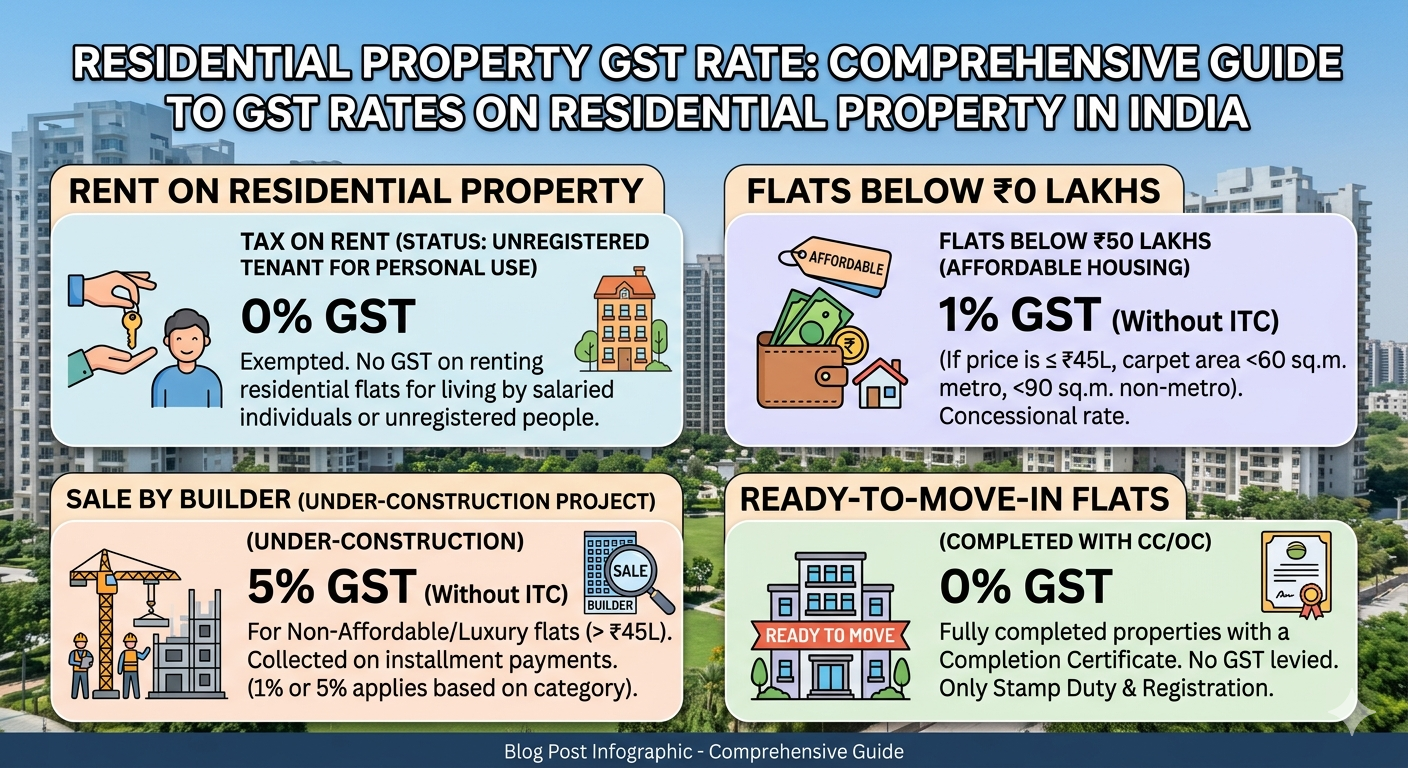

GST on Rent of Residential Property in India

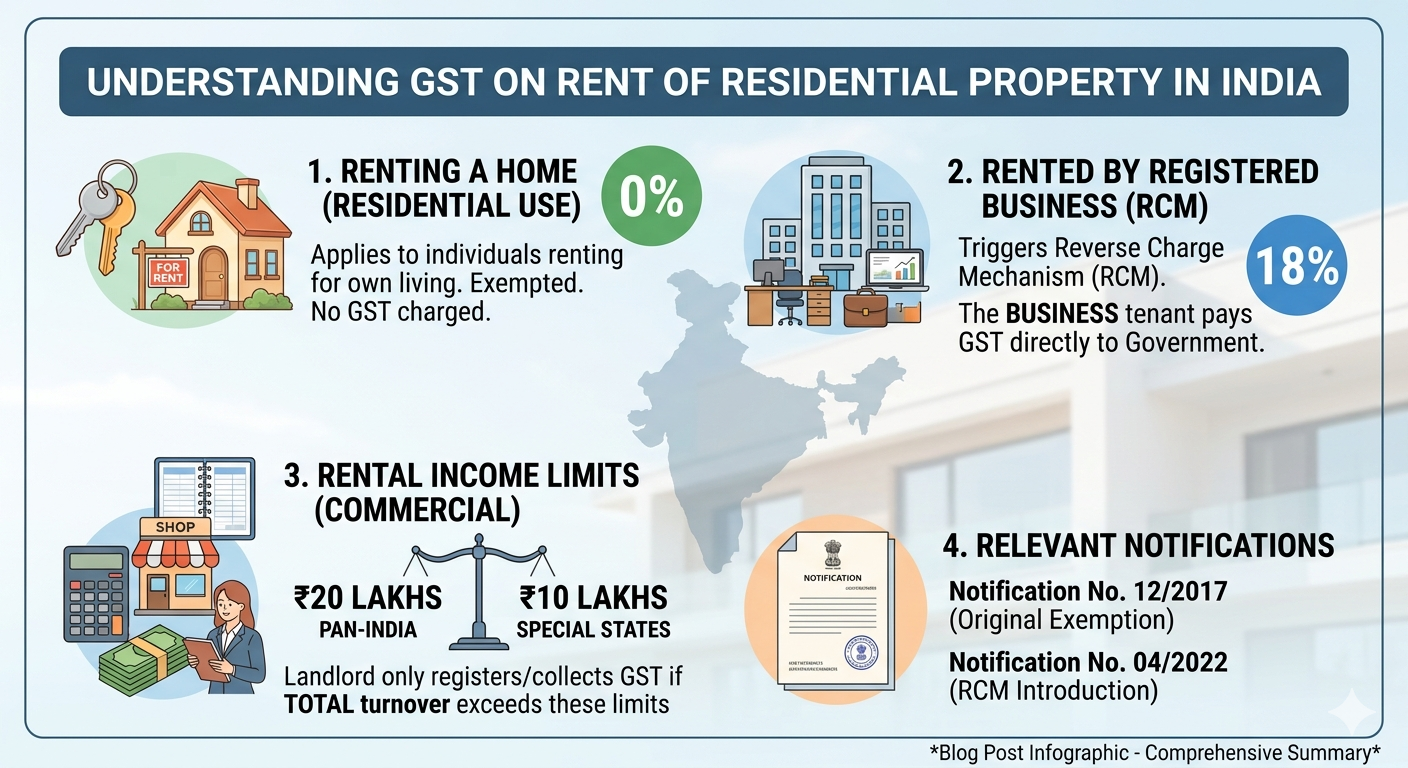

GST on Rent of Residential Property in India : Residential accommodation for people living in a residential property to breathe is exempt from GST. In contrast, in case the tenant is registered under GST (goods and services tax) and rents the property for business purpose (such as running corporate guesthouses or employee accommodation), an 18% GST will be applicable which will need to be borne by the tenant as a reverse charge mechanism (RCM).

Key GST Rules Breakdown

Personal Use: 0% GST is applicable if a person or family rents home/flat to reside in it. This is completely exempt from GST regardless of whether the landlord or tenant are GST registered.

Registered by business entity Renting of residential dwelling rent is 18% GST prime if the firm about company are partnership or proprietor companies. Here, the tenant pays the tax to the government directly due to Reverse Charge Mechanism (RCM).

GST is not applicable if you are an unregistered person renting (for business) a dwelling where the landlord is not registered.

Clarifications

Mixed use: Entities that only partially own the property with one half of its business for residential (like a bolthole) and the other part commercial.

Commercial Properties: This is the case when you rent a property that has been made only for commercial use (commercial shops, offices or warehouses) always attract 18% GST.

The application of Goods and Services Tax (GST) with respect to the lease/rent on a residential property only depends on who is a tenant and how he/she uses the property.

Here are the exact point-to-point breakdown of rules:

Let out to an unregistered person for use of the premises as a residence

GST Rate: 0% (Exempt)

In India, the law states that if a residential flat/house/apartment is rented out for living, to either a salaried individual or family or in fact any person who is not registered under GST for the sole purpose of personal habitation – then it will earn absolute tax exemption. No GST charged or paid by the landlord; tenant also pays no GST.

Leased Property to Corporate/Residential (meaning leased to a company or resident whose accounting is done under GST)

GST Rate: 18%

Mechanism: Reverse Charge Mechanism (RCM)

Rule: Scheduled residential property rent by other registered businesses / companies/business as per GST.

Who Pays? In RCM, this tax is not collected by the lessor. In this case, it is still the business that has registered itself as a tenant who is legally bound to pay the 18% GST directly to the government.

The Proprietorship Exception (Self-Residence)

GST Rate: 0% (Exempt)

Rule: Exception for a person even if the individual may be conducting a GST-registered sole proprietorship business but renting a residential house in his/her personal capacity solely for residential purpose would continue to be exempt. This holds true provided that they are not deducting the rent from their company accounts as a cost of running their business.

COMMERCIAL (Any Tenant)

GST Rate: 18%

Rule: If a residential property is leased out for commercial purposes (A clinic, boutique, start-up office, coaching center), then it loses the privilege of being considered as a residence under any aforementioned schemes. It is exactly just like renting a commercial property:

FCM (Forward Charge): As the landlord is registered on GST (since their total annual revenue is above ₹20 Lakhs), they are required to collect GST from tenant @ 18%.

Then, 18% GST is indirectly imposed when an unregistered landlord leases it out to a registered business for commercial purposes and the tenant pays this tax under Reverse Charge (RCM).

Quick Summary Matrix

| Landlord Status | Tenant Status | Purpose of Use | GST Rate & Applicable Mechanism |

| Registered / Unregistered | Unregistered (Salaried/Individual) | Residential (Living) | 0% (Exempt) |

| Registered / Unregistered | Registered (Company/Firm) | Residential (Guest house/Staff) | 18% under RCM (Paid by Tenant) |

| Registered / Unregistered | Registered Proprietor (Personal Cap) | Residential (Own Living) | 0% (Exempt) |

| Registered | Registered / Unregistered | Commercial (Office/Shop) | 18% under Forward Charge (Collected by Landlord) |

| Unregistered | Registered | Commercial (Office/Shop) | 18% under RCM (Paid by Tenant) |

For landlords, business owners and corporate tenants, grasping the convergence of Goods and Services Tax (GST) with rental property is crucial. An explicit, point-by-point outline that can function as clear, scannable text on your website blogs.

Input Tax Credit via GST on Rent of Residential Property Used for Commercial Purpose

If you have a property that is built for residential purpose (e.g. flat, bungalow) but is rented out to run a business (like your startup has an office there or it can be used as boutique/ clinic), then entire property completely loses tax exemption.

The Rate: It is charged a normal GST slab of 18%.

Tax Mechanism : Covered under Forward Charge Mechanism (FCM). The 18% GST are charged, collected and deposited by the landlord itself from tenant, in case the landlord is registered under GST.

Tax on Rent of Commercial Property

Earning rent from conventional commercial premises that includes retail shops, offices, warehouses and showrooms, is classified as a ‘supply of service’ under the GST law.

Standard Rate: 18% GST applies on total rent amount

Input Tax Credit(ITC): Tenants, who have a registered business may appropriately claim Input Tax Credit(ITC), 18% of the amount of GST paid on rent.

Relevant Notifications for GST on Residential Property Rent

The laws governing the renting of residences have been significantly altered by special orders from governments:

Basic Principle: As per Notification No. 12/2017-Central Tax (Rate), renting of a residential dwelling for use as residence was exempt from GST in full.

This unconditional exemption was revoked by the Notification No. 04/2022 & 05/2022-Central Tax (Rate) [effective from July 18, 2022]. It requires that GST should apply where a residential property is let to a registered person or entity.

Proprietor Relief: In order to protect consumers from unnecessary tax burdens, Notification No. 15/2022-Central Tax (Rate) clarified that renting a house in the personal capacity of the registered proprietor for self-occupation was still exempt (0% GST).

GST on Rent Of Residential Property Under RCM (Reverse Charge)

The Reverse Charge Mechanism (RCM) made a change in this direct way.

RCM applicability: RCM is triggered on automatically renting a residential dwelling to GST registered business entities (ex. corporate guest houses, staff quarters or company offices).

The Dynamic: The landlord does not charge GST and therefore does not collect. The registered corporate tenant is legally bound to compute the 18% GST and deposit it directly with the tax department instead.

GST on Rent of Commercial Property — Who Pays GST

Who has to pay tax is dependent on the registration of both parties.

For Scenario A (Registered Landlord → Any Tenant): The 18% GST is collected and paid by the Landlord under Forward Charge.

Scenario (B)Non-registered landlord $\rightarrow$ Registered tenant Tenant, has to pay the GST at 18% by himself to Government under Reverse Charge Mechanism of payment.

Scenario C — (Unregistered Landlord $»$ Unregistered Tenant): No GST paid by both parties

20% of ₹40 Lakhs = GST liability on ₹8 Lakhs on total rent income (₹10,000 × 12) year

Going above the baseline eligibility for tax exemptions changes rules of compliance more than 100%.

Compulsory Registration: The aggregate threshold of services is ₹20 Lakhs per year, which means that with an annual revenue of ₹40 Lakhs from commercial tenancy, the owner must register for GST.

GST charged by the landlord on inrental invoice : 18% This effectively means on a yearly rental income of ₹40 Lakh, the total GST collection and outgo through remittance in the financial year is to the tune of ₹7,200,000.

In India, is GST exempt on Rent of Residential Property?

The rule also continues to be very consumer friendly at its core: if you’re concerned about the rental of homes on an everyday basis.

Living Exemption: If a regular person or an employee who pays salary rents an apartment only to live in, ~no GST (0%). This exemption does not get affected by quantum of rent and continues even if the tenant, being unregistered, is using it as a residence.

The Dictate Of GST On rental Limit (Exemption Thresholds)

Landlords will not be required to register and pay tax unless these following turnover thresholds are exceeded:

Standard Aggregate Threshold: 20 Lakhs per annum. As long as your entire taxable turnover for all commercial rentals and other business activities is kept at or below this threshold, you do not have to charge GST.

Specialised Category states : ₹10 Lakhs per annum (valid only in several north-eastern and hill states).

Important Caveat: This combination is a total limit of all taxable business revenue together—So if you combine anything such as a very small commercial shop rent with different turnover from another retail business, this will be added up to determine whether you are above that limit.

The applicable GST on house rent is predetermined by the type and use of property, coupled with the registration status of tenant. GST is wholly exempted from residential property rented out for human habitation. In contrast, the hiring of a residential or commercial property to conduct business will qualify for an 18% GST, which usually falls upon the tenant through the Reverse Charge Mechanism (RCM).

| Property Type | Tenant’s Usage & Registration Status | GST Rate | Who Pays / Exemption Status |

|---|---|---|---|

| Residential | Personal use (Unregistered tenant) | Nil | Fully exempt |

| Residential | Used for business by a GST-registered tenant | 18% | Paid by the tenant via RCM |

| Commercial | Any usage (Shops, offices, godowns) | 18% | Paid by the tenant via RCM |

Key Details & Scenarios

Residential Exemption — If you live in and rent out a house or an apartment for yourself, the rent is not used to calculate your GST. It does not matter if the landlord is registered under GST or not.

Business Use (18% Granularity): An 18% GST is imposed if a residential house is rented to a registered proprietor under GST for official use/business purposes such as either a guesthouse for the corporation or an office.

Input Tax Credit (ITC): If you are a business making a payment of rent for the say commercial or business-use properties, you can claim back the 18% GST paid to benefit from ITC and reduce your effective rental obligation.

Landlord Registration Limits

Landlords do not collect GST on personal residential rent but their rental income still faces standard Income Tax on Rental Income. A landlord whose aggregate taxable income in a financial year is above ₹20 lakh (or ₹10 lakh for special category states) from all of India, including rental income received for commercial property, must register under the GST portal on a mandatory basis.

Commercial Property GST Rate

The Complete GST Rules & Rates on Commercial Property in India for the Master Guide.