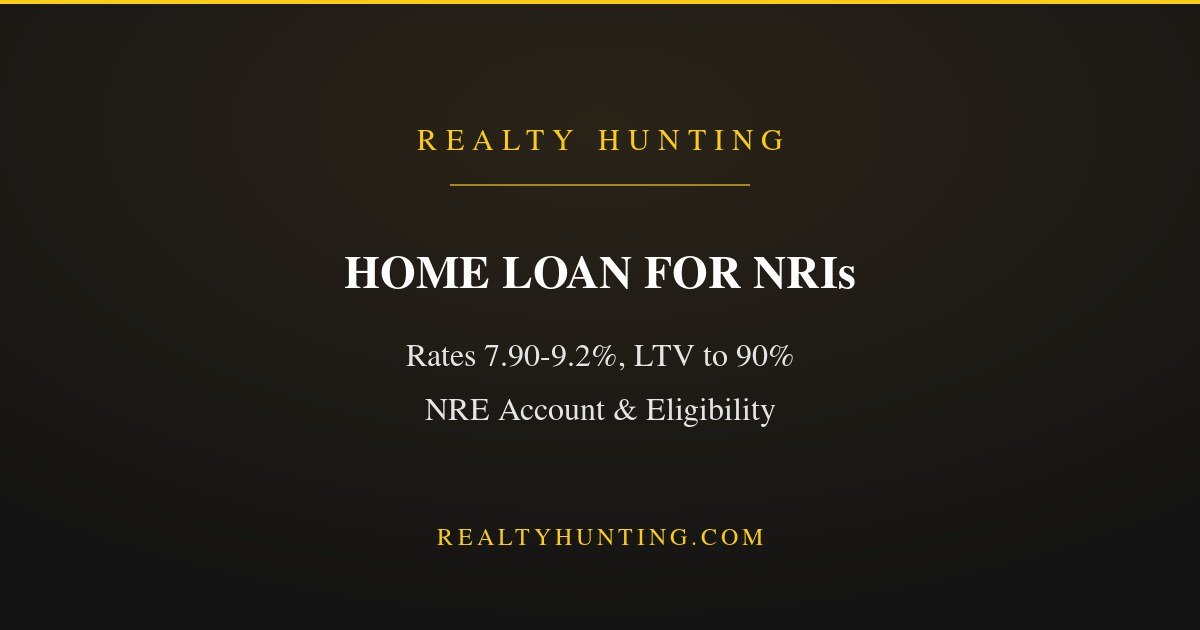

Home Loan for NRIs in India: Rates and Rules

An NRI buying property in India can absolutely take a home loan here, and often should, since it lets you keep your foreign savings invested while an Indian bank funds the purchase. But NRI home loans come with their own rates, limits, and one rule that trips people up: the EMI must be paid from the right account. This guide covers NRI home loans in India for 2026, with the real numbers.

NRI home loan rates and terms

| Feature | Detail (2026) |

|---|---|

| SBI NRI rate | Around 8.45% to 9.2% |

| HDFC NRI rate | From 7.90% (up to 9.7%) |

| Loan-to-value (LTV) | Up to 90% for small loans, 75-80% for large |

| Tenure | Up to 20-30 years, limited by age at maturity |

| EMI account | Must be serviced through an NRE or NRO account |

Rates are from current bank data, mid-2026, and are floating, moving with the RBI repo rate of 5.25 percent. NRI rates are broadly in line with or slightly above resident rates. Banks fund up to 90 percent for loans up to ₹30 lakh, dropping to 75-80 percent for larger loans, similar to resident LTV rules. Confirm your exact rate and terms with the bank.

Who is eligible

NRI home loans are open to Non-Resident Indians, OCIs, and PIOs. Banks typically want you to have worked abroad for at least two years, with at least one year with your current employer, and a stable income. A salary in a hard currency like US dollars, pounds, or dirhams is viewed more favourably than one in a weaker currency. Documentation is heavier than for residents: passport and visa, overseas and Indian address proof, income and employment papers, often attested, and a power of attorney for someone in India to act on your behalf.

The account rule you must follow

Under FEMA rules, an NRI home loan cannot be serviced from just any account. The EMI must be paid through your NRE or NRO account, using your foreign earnings routed to India, or from rental income on the property. Set this up correctly at the start, since paying from the wrong account creates compliance problems. A power of attorney to a trusted person in India helps manage the loan, registration, and property remotely.

Buying and later selling as an NRI

A home loan is only one part of the NRI property picture. For the purchase side, weigh the rupee loan against bringing money from abroad, and factor currency movements. When you eventually sell, the tax and repatriation rules are stricter, higher TDS and the need for a lower-TDS certificate, covered in our NRI selling property guide. For the broader buying strategy, see our NRI property investment guide.

Loan in India or funds from abroad?

A key decision for an NRI buyer is whether to take a rupee home loan in India or simply bring money from abroad and buy outright. A loan lets you keep your foreign savings invested, potentially earning more than the loan's interest cost, and it gives you a rupee liability against a rupee asset, which is a natural currency hedge. Bringing funds avoids interest altogether but exposes you to exchange-rate timing and locks up capital. Many NRIs take a partial loan: a healthy down payment from abroad to keep the loan small, then a rupee loan for the balance serviced from Indian rental income or routed foreign earnings. The right split depends on your rate abroad, your investment returns, and your view on the rupee, so run the numbers both ways before deciding.

Frequently asked questions

Can an NRI get a home loan in India?

Yes. NRIs, OCIs, and PIOs can take home loans from Indian banks, with rates around 7.90 to 9.7 percent in 2026 and funding up to 90 percent for small loans.

What is the interest rate on an NRI home loan?

Around 8.45 to 9.2 percent at SBI and from 7.90 percent at HDFC in mid-2026, floating and moving with the RBI repo rate. NRI rates are broadly in line with resident rates.

How is an NRI home loan EMI paid?

Through your NRE or NRO account, using foreign earnings routed to India or the property's rental income, as required under FEMA. It cannot be paid from any other account.

What is the maximum tenure for an NRI home loan?

Up to 20 to 30 years depending on the bank, but limited by your age at maturity, often capped around 60 to 70 years.

What documents does an NRI need for a home loan?

Passport and visa, overseas and Indian address proof, income and employment papers, often attested, and a power of attorney for someone in India to act on your behalf.

Do NRIs pay higher interest than residents?

Broadly in line, sometimes slightly higher, with heavier documentation and a lower loan-to-value on large loans. The main differences are the account rule and paperwork, not a big rate gap.

An NRI home loan lets you buy in India while keeping your foreign savings invested, at rates around 7.90 to 9.2 percent in 2026, funded up to 90 percent for small loans. Set up the NRE or NRO account for EMIs, keep a power of attorney ready, and plan the sale-side tax early. Read more on our blog. Rates are indicative mid-2026 figures, so confirm with the bank.