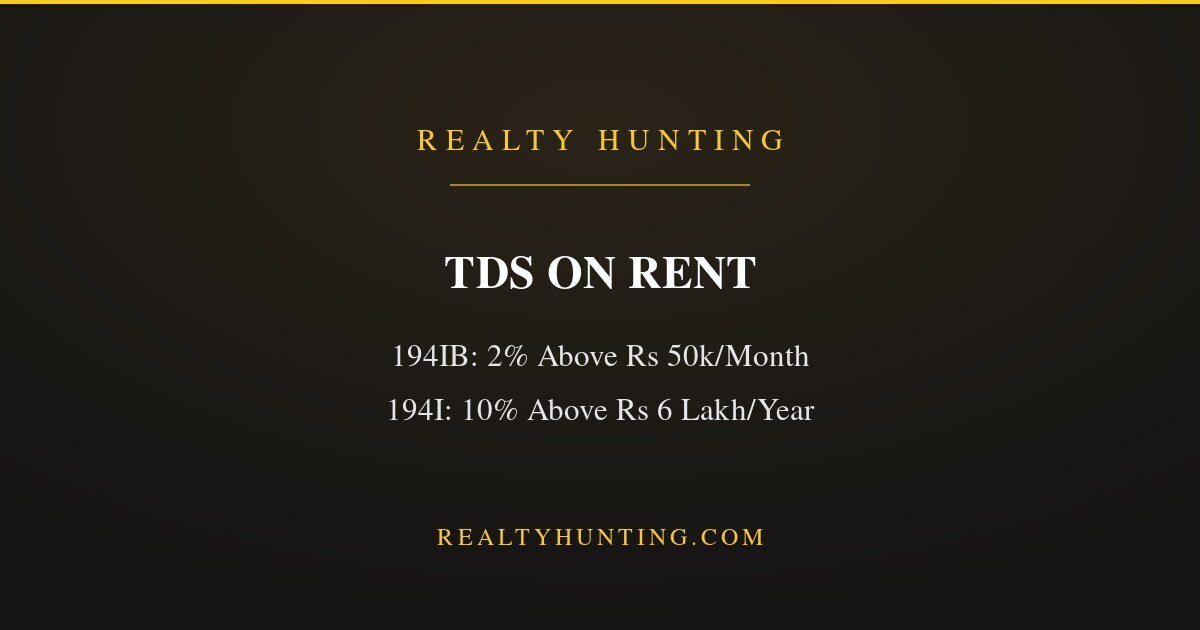

TDS on Rent: Section 194I and 194IB Rules

Many tenants and companies do not realise that paying rent above a certain amount comes with a tax duty: you must deduct TDS on the rent and deposit it with the government. Miss it and the penalty falls on you, the payer, not the landlord. This guide explains TDS on rent in 2026, the thresholds, the rates, and who has to deduct, under Sections 194I and 194IB.

The two sections and their rules

| Section | Who deducts | Threshold | Rate |

|---|---|---|---|

| 194IB | Individuals / HUFs not under tax audit | Rent above ₹50,000 per month | 2% |

| 194I | Companies, firms, audited entities | Rent above ₹6 lakh per year | 10% (building/land) |

Rates and thresholds are current for 2026. So an ordinary salaried tenant paying more than ₹50,000 a month must deduct 2 percent TDS under 194IB, while a company or business paying annual rent above ₹6 lakh deducts 10 percent under 194I. If the landlord does not provide a PAN, the rate jumps to 20 percent.

Section 194IB: for individual tenants

If you are an individual or HUF not subject to tax audit and your rent exceeds ₹50,000 a month, you must deduct 2 percent TDS. This rate was reduced from 5 percent to 2 percent with effect from October 2024, so it is now a small deduction. You deduct it once a year, or in the last month of the tenancy, and deposit it using a simple challan-cum-statement, no separate TAN is needed for 194IB. Give the landlord a TDS certificate afterwards.

Section 194I: for businesses

Companies, firms, and individuals or HUFs under tax audit deduct TDS under 194I when annual rent for land, buildings, or furniture exceeds ₹6 lakh. The rate is 10 percent for land and buildings and 2 percent for plant and machinery. This threshold was raised from ₹2.4 lakh, so fewer small business tenancies are now caught. Businesses deduct monthly and need a TAN to deposit the TDS.

Practical rules to remember

- No PAN, higher TDS: if the landlord does not furnish a PAN, deduct at 20 percent, so always collect the PAN.

- GST excluded: where GST is shown separately in the rent invoice, deduct TDS on the rent excluding GST.

- Deposit on time: late deposit attracts interest and penalty on you, the deductor.

- Give the certificate: the landlord needs the TDS certificate to claim credit in their return.

For landlords, this TDS is not a cost but a prepaid tax you claim credit for, so keep the tenant's certificate. If you are weighing renting against buying, our rent versus buy guide runs the numbers, and tenants claiming HRA should read our HRA exemption guide.

A worked example for a tenant

Suppose you are a salaried individual renting a flat at ₹60,000 a month. Since this exceeds the ₹50,000 threshold, Section 194IB applies and you must deduct 2 percent TDS. Over a year that is ₹7,20,000 in rent, so ₹14,400 of TDS, which you deduct, typically once in the last month of the year or the tenancy, and deposit with a challan-cum-statement, no TAN needed. You pay the landlord the rent net of this ₹14,400 in that month, and give them a TDS certificate so they can claim the credit. If the landlord has not given you their PAN, you would have to deduct at 20 percent instead of 2, a huge difference, so always collect the PAN at the start of the tenancy. Miss the deduction entirely and the interest and penalty land on you, not the landlord, which is why tenants above the threshold should set this up correctly from the first month.

Frequently asked questions

Do I have to deduct TDS on my house rent?

Yes, if you are an individual paying more than ₹50,000 a month, you deduct 2 percent under Section 194IB. Businesses paying annual rent above ₹6 lakh deduct 10 percent under 194I.

What is the TDS rate on rent in 2026?

Two percent for individuals under 194IB, and 10 percent for land and buildings under 194I for businesses. Without the landlord's PAN, it rises to 20 percent.

What is the threshold for TDS on rent?

Rent above ₹50,000 a month for individuals under 194IB, and annual rent above ₹6 lakh for companies and audited entities under 194I.

Do I need a TAN to deduct TDS on rent as an individual?

No, under Section 194IB individuals deposit the TDS using a challan-cum-statement without a separate TAN. Businesses under 194I do need a TAN.

Is TDS deducted on the rent including or excluding GST?

Where GST is shown separately in the invoice, TDS is deducted on the rent amount excluding GST.

What happens if I do not deduct TDS on rent?

The penalty and interest fall on you, the payer, not the landlord. So deduct and deposit on time if your rent crosses the threshold, and always collect the landlord's PAN.

If your rent crosses ₹50,000 a month as an individual, or ₹6 lakh a year as a business, you must deduct TDS, 2 percent or 10 percent, and deposit it, or the penalty is yours. Collect the landlord's PAN, exclude GST, and give the TDS certificate. Read more finance guides on our blog. Rules are current for 2026, so confirm specifics with a tax advisor.