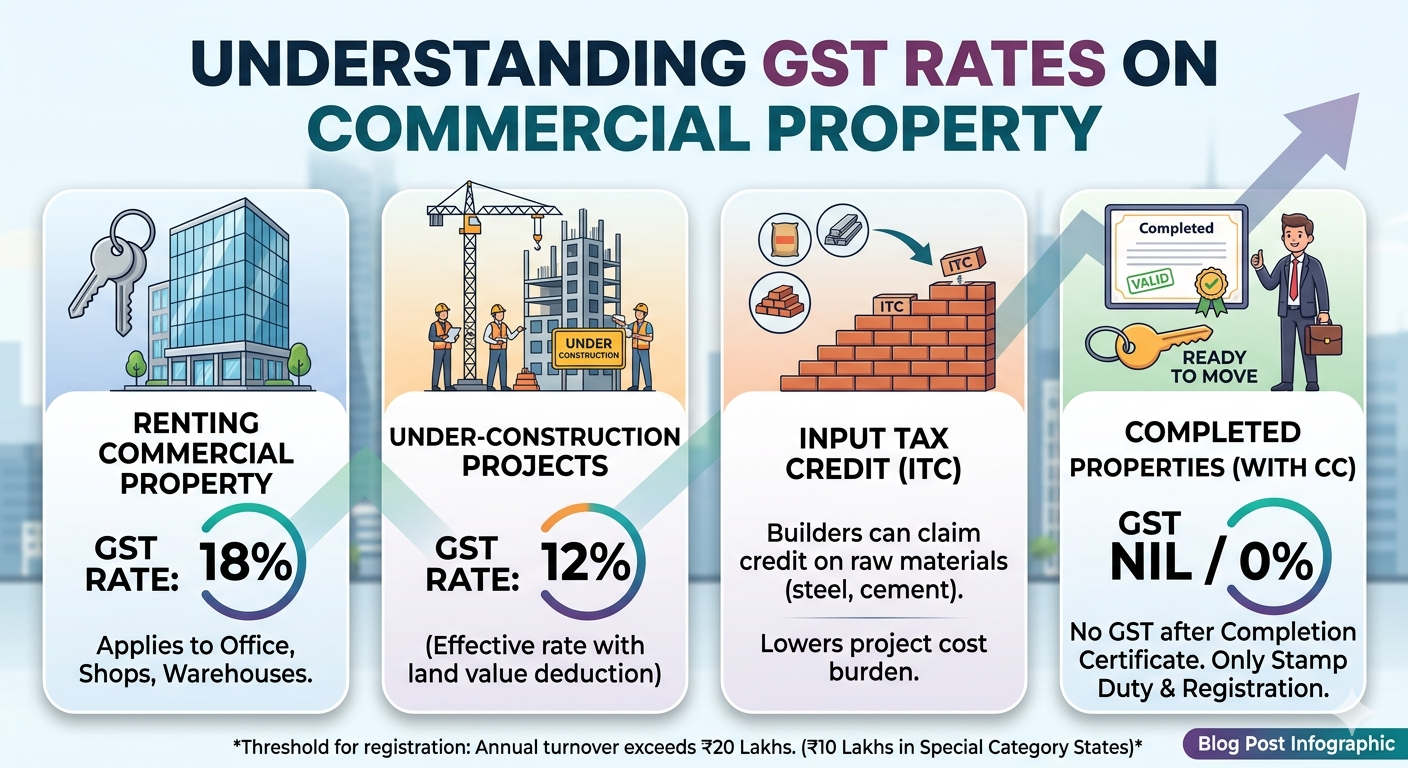

Commercial Property GST Rate : The GST rates for commercial property in India may vary based on the type of transaction. The GST on the renting or leasing is 18%. Commercial properties under construction can also avail the Input Tax Credit (ITC) at the rate of 12%. For ready-to-move or completed properties, zero per cent GST is applicable (only stamp duty applies).

| Transaction Type | GST Rate | Details |

|---|---|---|

| Rent / Lease | 18% | Landlords must charge 18% on commercial rent. Mandatory to register for GST if total rental income exceeds ₹20 lakh/year (₹10 lakh in special category states). |

| Under-Construction Sale | 12% | Buyers pay 12%, but developers can claim Input Tax Credit on construction expenses. |

| Ready / Resale (Completed) | 0% | No GST is applicable on completed commercial properties that already have a completion certificate. |

Important Rules to Note:

Input Tax Credit — Businesses and registered tenants remitting the 18% Goods & Services Tax on commercial rent can usually claim ITC, which decreases their overall tax obligation.

Reverse Charge Mechanism/(RCM):If the landlord has not GST registration which is an unregistered individual and the tenant(tenant) is a business registered under GST then it will be liable to pay directly to the government under RCM.

Residential Properties: The commercial GST rate of 18% would still apply when a residential unit is rented (as part of the business) to a business or corporate entity.

To read the rules & regulations, registration process in brief visit IndiaFilings GST on Rent Guide or ClearTax GST on Real Estate Services portal for filed dedicated in depth articles.

The GST applicable for commercial property purely depends upon the transaction you are undertaking i.e. under-construction purchase of the said property, renting it out or new ready to move in purchase..

Highlighted below are the standard GST rates levied on commercial properties:

Renting or Leasing Commercial Property

GST Rate: 18%

Scope: This applies to rentals of office space, retail shop, showroom and warehouse.

Threshold Rule: A landlord is mandated to register and charge GST only if his/her annual aggregate turnover (inclusive of rental income and business revenue) exceeds ₹20 Lakhs (₹10 Lakhs in special category states).

RCM (which requires the GST registered business entity to pay an 18% GST directly to the government, if the landlord does not have a GST registration and therefore cannot charge and collect such a tax).

Purchase of Under-Construction Commercial Property

GST Rate: 12% (but effectively calculated at 18%-1/3rd deduction in land value) or 18% of only 67% of the entire property value.

Input Tax Credit (ITC): Developers/builders are entitled to take Input Tax Credit on Raw Materials (cement, steel) and services used during construction thus reducing costs.

Mixed Development Projects: A commercial shop/office is treated as a part of the Residential Real Estate Project (RREP) where its carpet area does not exceed 15% of the total project area, a lower GST rate of 5% (without ITC) will be applied.

Purchase of Ready-to-Move-In Commercial Property

GST Rate: 0% (Exempt)

Applicability: GST is not applicable in the case of buying an already conferred commercial property, that has its Completion Certificate or first occupancy done. Normal state stamp duty and registration fees are applied.

Commercial Property Summary GST Table

| Transaction Type | GST Rate | Input Tax Credit (ITC) Availability |

| Commercial Rent / Lease | 18% | Available to the tenant (if registered) |

| Under-Construction Purchase (Standard) | 12% | Available to the developer |

| Under-Construction Purchase (In Residential Project <15%) | 5% | Not Available |

| Ready-to-Move / Completed (with CC) | 0% | Not Applicable |

The Complete GST Rules & Rates on Commercial Property in India for the Master Guide.

The Goods and Services Tax (GST) is an indirect tax that the developers, buyers, investors, or landlords finding it difficult to comprehend. GST On Commercial Property – A Point By Point Guide for Your Website Blog This a block entry on commercial property GST

GST on Business Home in Progress

The law states that any investment where the buyer purchases a commercial shop, office space or showroom which is still under construction will be a supply of service (construction service)transaction wherein you would be dealt with as either an abiding near landlord or potentially even first tenant.

Rate: The standard GST rate is 12%.

What it does: Your real service rate is at 18% percent but the government gives you a flat deduction of 1/3rd (33.33%) against the value of your land. Hence, 12 % with respect to the whole contract value is settled for as an effective tax rate.

Payment Milestone: All payments made to the developer before physical completion of the building (including demand notes, booking amounts and construction-linked payments)

Question: Whether GST is applicable on the rent of commercial property?

Thus, leasing or sub-leasing any immovable commercial property for business use is a taxable supply of services as per Goods and Services Tax laws.

Standard Rate: The rental amount is charged 18% GST at a flat rate.

Exemption limit of ₹20 Lakh: A landlord only needs to register and charge this 18% tax under GST if his aggregate annual business turnover (including rental income from all properties along with other business receipts) exceeds the ₹20 Lakhs limit (₹10 Lakhs for special category states).

Reverse Charge Mechanism (RCM) Rule: No tax is collected by the registered landlord from an unregistered landlord, which leases out its commercial space to a GST-registered company. The tenant is instead obliged to pay the 18% GST directly to the exchequer under RCM. Tenants can take these back as an input tax credit (ITC) later on.

GST on Sale of Commercial Property (Ready v/s Ready)

Applicability of GST on sale of a commercial asset entirely depends on the completion status of the building:

Taxable at 12%: Before Completion Certificate (CC) GST applies if payments occur as the structure is being constructed.

Post Completion Certificate (Ready to-Move):0% (exempted). In the event you acquire a commercial building that is fully constructed which has received its CC or was previously occupied, it would be treated as a transfer of immovable property & not service, hence chargeable to GST. No GST is levied.

Resale Properties: 0% (Exempt). I.e. new commercial assets are taxed under GST but second-hand or resale commercial assets do not attract GST simply because they are already finished entities in their own right. Disclaimer: Stamp duty and registration charges continues to be relevant on the ultimate property registry.

India Commercial Property GST Rate: Summary And Quick Reference

| Property Scenario / Transaction Type | Effective GST Rate | ITC Eligibility |

| Under-Construction Office/Retail Shop | 12% | Allowed for Developers |

| Commercial Space within a Residential Project (<15% area) | 5% | Blocked (No ITC) |

| Renting / Leasing out Commercial Space | 18% | Allowed for Registered Tenants |

| Ready-to-Move Commercial Property (With CC) | 0% (Exempt) | Not Applicable |

| Sale of Pure, Undeveloped Land | 0% (Exempt) | Not Applicable |

GST Rate Calculator (Formula & Example for Commercial Property)

But to keep the cost in check, GST calculation needs to have land value component deducted from it so that you are not made to pay more than what is due.

The Calculation Formula:

-

Exempted Land Value = Total Agreement Value $\times \left(\frac{1}{3}\right)$

-

Taxable Value of Construction = Total Agreement Value $-$ Exempted Land Value

-

GST Payable = Taxable Value of Construction $\times 18\%$

Practical Example:

Suppose you book an under-construction retail shop in Gurgaon for a total agreement value of ₹1 Crore.

Land Deduction (1/3rd): ₹33,33,333

Taxable Construction Base (67%): ₹66,66,667

GST Component (18% of ₹66,66,667): ₹12,00,000

Total Property Cost (including GST): ₹1,12,00,000

(Note: This simplifies directly to a flat 12% on the total ₹1 Crore agreement value).

Pointwise GST on Sale Before Completion Certificate

There are strict regulations on selling unit that is still going through construction. Here are some key compliance takeaways for your website readers:

Who has to collect and pay the 12% GST @ 2019 Base RateIt is a simple clause, which states that normally the builder/developer will have the obligation to collect and deposit with tax authorities.

GST becomes due the instant first booking advance is very cleared, irrespective of whether or not any construction activity has commenced on site at all — Booking Amount Liability

It is in a phased manner: Though under construction, if you buy, GST will be levied on every instalment milestone invoice raised by the builder.

GST Rate on Commercial Property Without Input Tax Credit

For developers, Input Tax Credit (ITC) enables them to deduct the GST they have paid on raw materials (such as cement, steel, and luxury fittings) from the final GST bill presented to the buyer. However, there is an exception for which a lower rate applies without this advantage:

Commercial Spaces in Residential Projects — whether ITC available is based on the type of regulation selling a commercial or retail shop inside the typically RREP (Residential Real Estate Project). As long as each unit does not exceed 15% of total carpet room, the developer cannot take an ITC.

The Rate: In this particular case, it is a 5% concessional GST without ITC on the buyer.

Commercial Property Sale by Individual — GST

So what happens if a person who is not a real estate developer goes into some commercial asset and he decided to sell it?

Selling completed property: If a person sellout a commercial property which is already having Completion Certificate GST does not trigger. It falls outside the ambit of GST, and only the seller pays Long Term or Short Term Capital Gains Tax under the Income Tax Act.

Supply of Rights in respect of Under Construction Allotment (Assignment Deed): Transfer or sell the right, title or interest (as defined under Section 54(b)) to an under-construction commercial unit to another buyer before obtaining possession or CC would be a supply of right to land/space. The transaction may fall under the 12% GST slab and individual would have to check for temporary registration or structured invoicing depending on the commercial nature of regular business volume.