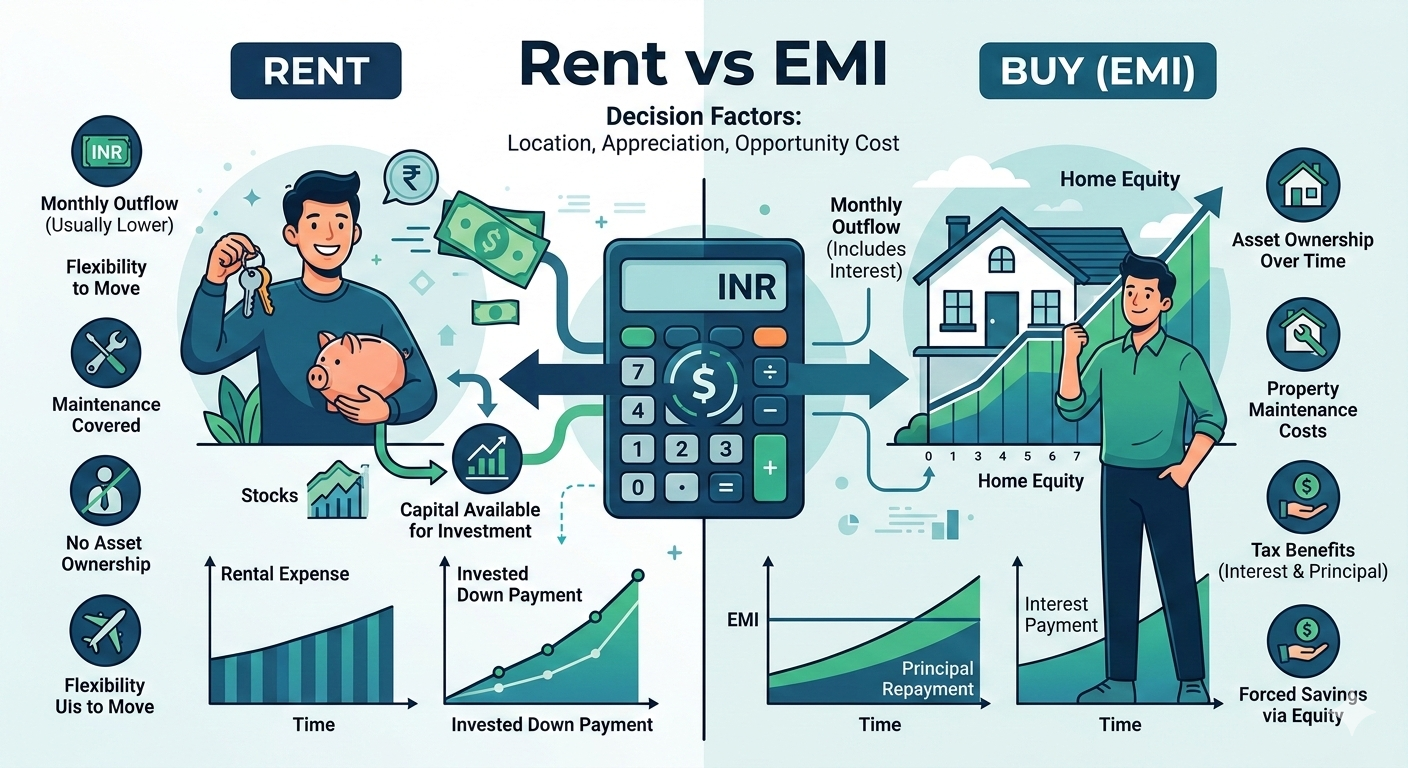

Paying rent Vs paying EMI (mortgage) is one of the common financial dilemma. It’s not just about the monthly outflow; it’s also opportunity cost and asset building.

The Comparison Table

Here is how the two typically stack up over a 10 to 15-year horizon:

| Feature | Renting | Buying (EMI) |

| Monthly Outflow | Usually lower than EMI. | Usually higher (includes interest). |

| Asset Ownership | None. | You own the property eventually. |

| Flexibility | High (easy to move for jobs). | Low (selling a house takes time). |

| Maintenance | Handled by the landlord. | Your responsibility & cost. |

| Tax Benefits | HRA (if applicable). | Interest & Principal deductions. |

| Wealth Gap | Depends on where you invest the “savings.” | Forced savings via home equity. |

How to Calculate the “Winner”

The true “cost” of renting isn’t the rent you pay; it’s what you do with the money you didn’t spend on a down payment. On the other hand, some parts of buying — interest, property taxes, maintenance — come with a price tag attached.

The Rent-to-Buy Ratio

A quick rule of thumb:

Price-to-Rent Ratio = Home Price / Yearly Rent

Under 15: Buying may be the better option.

15 to 20: That’s a flip of the coin; it goes either way depending on what your objectives are.

More Than 20: Renting is often the wise financial play.

The Opportunity Cost Math

If you rent, you have a lump sum (the down payment) that could get locked in to the stock market/mutual funds.

Scenario A (Renting) : (Rent + Rent Appreciation) – (Investment Appreciation of Down Payment).

Scenario B (Buying): (EMI + Maintenance + Taxes) – (Property Appreciation).

Essential Variables to Consider

Make sure you have these numbers handy before running the numbers:

Increased Property Value: Is your area’s home value increasing 5%, 10%?

Investment Returns: Might you make in the market 12 percent on your down payment?

Loan Interest Rate: Just a 1% difference in your mortgage can make you pay or save thousands over 20 years.

Rental Inflation: Rent typically rises 5-10% per year.

Pro Tip: If more than 40% of your take-home pay goes toward your EMI, the “peace of mind” of owning a home might just leave you stressed.

The “Rent vs. EMI” debate in Gurgaon (2026) has changed with a massive spike in property prices and rentals. Although the city has always been a “renter’s paradise,” low rental yields kept prices down, but new infrastructure like the Dwarka Expressway has tipped the math.

The 2026 Gurgaon Snapshot

Rental Yields: Residential yields have risen to between 3% –5%(versus the traditional 2.5%), particularly in gated societies.

Appreciation: In prime corridors (Golf Course Ext, Dwarka Expressway), the growth stands in the range of 8% – 12 percent every year.

Home Loan Rates: Most borrowers at 7.5% — 8.5% range right now

Comparison: 3BHK in New Gurgaon / Dwarka Expressway

Assumed Property Value: ₹2.5 Cr | Down Payment: ₹50 Lakh (20%)

| Feature | Renting (Monthly) | Buying (EMI) |

| Outflow | ₹65,000 – ₹85,000 | ₹1.5 Lakh – ₹1.7 Lakh |

| Tax Benefits | HRA (approx. ₹15k-25k savings) | Sec 24 & 80C (approx. ₹7k-10k savings) |

| Maintenance | Included in rent (usually) | ₹8,000 – ₹12,000 (Extra) |

| Net Monthly Cost | ~₹60,000 | ~₹1.6 Lakh |

Which is better for you?

Choose RENT if:

You value liquidity: You would instead invest that ₹50 Lakh down payment in a portfolio generating 12%+ (Mutuals/Equity). In Gurgaon, the “gap” between rent and EMI remains sufficiently widened, that whenever the surplus is invested elsewhere, over 80% of time it outperforms real estate.

Job volatility: You work in Tech or Consulting, and may need to relocate to Bangalore, Dubai or Europe within 3 years.

The lifestyle of “luxury”: The rent of a ₹4 Cr penthouse starts at ₹1.2 Lakh/month, EMI amount to pay if taking an equivalent apartment on loan is almost ₹3 Lakh. Renting gives you the opportunity to live “above your means.”

Choose BUY (EMI) if:

You want stability: You are a settled professional with family and do not want to have a 10 per cent rent increase every year, the norm in premium sectors of Gurugram.

Long-term horizon: You’re in it for 7+ years Gurgaon’s infrastructure is maturing, and the capital appreciation from a well-located property hardly justifies your total interest outgo over 10 years.

Forced Saving: You are not regular at saving; EMI makes sure you build an asset instead of spending your surplus.

The “Golden Rule” for Gurgaon 2026

If the Price-to-Rent Ratio in your specific sector is above 25, continue renting. For example, if a flat costs ₹3 Cr and rents for ₹1 Lakh/month ($Price/Annual Rent = 300/12 = 25$), the market is slightly “overheated” for buyers, making renting more efficient.

“Rent is money down the drain”: Is this true?

Not necessarily. In a high-growth market like Gurgaon, when you pay ₹80,000 in rent but invest your ₹50 Lakh down payment in an equity fund that earns between 12 and 14% return on investment, the value of the investment is making more than what you “save” on the rent. Renting is in effect “purchasing” the flexibility to put your capital elsewhere.

Which is the “5% Rule” for Gurgaon?

The 5% rule is a simple mathematical shortcut:

Add up the yearly expense of homeownership (Property Tax + Maintenance + Cost of Capital/Interest).

This is generally around 5% of total property value in Gurgaon.

If you can rent the same house for less than 5% of its market value each year, renting is the better financial choice.

What does the math look like with Gurgaon’s 10% annual rent increases?

How renters deal with the “silent killer” Conversely, rent in sectors such as 59, 65 or 102 increases at a rate of about 10% every year, even thought an EMI is fixed for the next two decades.

Year 1: Rent is ₹70,000.

Year 10: Rental is ~₹1.65 Lakh. In Year 10, for instance, your “cheap” rent may well be more than what your EMI would have been fixed at.

Does buying in Gurgaon help you save taxes?

Yes, but they are capped. According to the Indian Income Tax Act:

Section 24(b): Interest paid (Self-occupied) deduction of up to ₹2 Lakh.

Section 80C: Deduction on principal repayment up to ₹1.5 Lakh For a ₹2.5 Cr home, all this amounts to relatively small benefits compared to your total interest payments, but you do end up getting a marginal “discount” on your effective EMI.

What are the “hidden costs” of purchasing in Gurgaon?

However, many buyers overlook these at the time of calculating their EMI:

NOTE: What follows are various charges associated with buying your flat in India. Direct taxes are Stamp Duty & Registration (~5-7% of property value; e.g ₹12-17 Lakh on a ₹2.5 Cr flat)

Interest-free Maintenance Security (IFMS): A lump sum amount paid to the builder as deposit.

GST: 5% on under-construction properties (Zero for Ready-to-Move)

Maintenance: In a premium society, this could be ₹8,000 to even ₹15,000 per month — which is like a “permanent rent” that you pay even after the loan period is over.

Summary Table: The Deciding Factor

| If your priority is… | The Winner is… |

| Lowest Monthly Outflow | Rent |

| Wealth Creation (Long term) | EMI (Buy) |

| Portfolio Diversification | Rent (Invest elsewhere) |

| Emotional Security | EMI (Buy) |

1. “Is it better to buy an under-construction property to save on EMI?”

In Gurgaon (especially along the Dwarka Expressway), buying under-construction can be a double-edged sword:

-

The Pro: You often get a lower price per square foot and staggered payments (CLP or PLP plans), which feels easier than a massive EMI from Day 1.

-

The Con: You pay Rent + Pre-EMI (interest on the disbursed amount) simultaneously. If the builder delays possession by 2 years (common in Gurgaon), your “savings” evaporate into double housing costs.

-

2026 Reality: With RERA being stricter, timelines are better, but Ready-to-Move (RTM) properties are currently commanding a 15-20% premium because they eliminate this “double-pay” risk.

2. “Should I buy a plot/floors or an apartment in a high-rise?”

-

Plots/Deen Dayal Jan Awas Yojana (DDJAY): These have seen the highest appreciation in Gurgaon (Sectors 92, 95, 88). If your goal is wealth creation, buy a plot.

-

Apartments: If your goal is lifestyle and security (power backup, gym, club), pay the EMI for a high-rise. Note that apartments depreciate in structure over 20-30 years, whereas land (plots) usually does not.

3. “What is the ‘Opportunity Cost’ of the Stamp Duty?”

In Haryana, Stamp Duty is roughly 5% for women and 7% for men.

On a ₹3 Crore apartment, you are paying ₹15–21 Lakh just to the government.

If you invested that same ₹20 Lakh in a Nifty 50 Index Fund for 10 years at a 12% return, it would grow to nearly ₹62 Lakh. When you buy, you lose this potential growth immediately.

4. “Can I use my HRA and Home Loan benefits together?”

Yes. This is a popular “hack” in Gurgaon:

-

If you buy a house in Sector 82 but work and rent a place near Cyber Hub (Sector 24) to save on commute, you can claim both the HRA tax exemption and the Home Loan interest/principal deductions.

-

This significantly tilts the math in favor of Buying because your tenant in Sector 82 pays part of your EMI, while the government “subsidizes” your tax outgo.

5. “What happens if the Gurgaon ‘Bubble’ bursts?”

Gurgaon has seen “flat” periods (2014–2019). If you buy at the peak (like now in early 2026) and prices stagnate:

-

The Renter: Can move to a cheaper area or negotiate rent down.

-

The Owner: Is stuck with a high EMI on an asset that isn’t growing.

-

The Buffer: Only buy if you plan to stay for 7+ years. Real estate cycles in Gurgaon are long; time usually heals a “bad” entry price.

6. “Is the ‘Rental Yield’ higher in Furnished vs. Unfurnished?”

In areas like Golf Course Road or DLF Phase 1-4, furnishing a 2BHK/3BHK can cost ₹10–15 Lakh but can increase rent by 20-30%.

-

If you are an investor looking to offset your EMI, fully furnished units in Gurgaon often bridge the gap between Rent and EMI much faster than bare shells.

Summary: The “Gut Check” Test

Ask yourself these three questions:

-

Am I staying in Gurgaon for at least 5 years? (If No $\rightarrow$ Rent)

-

Is my total debt (EMI + others) less than 45% of my pay? (If No $\rightarrow$ Rent)

-

Do I have a 6-month emergency fund after the down payment? (If No $\rightarrow$ Rent)

1. “I’m seeing 20-30% rent spikes in Gurgaon. Is my EMI safer?”

Yes. In 2026, many tenants in sectors like 65, 70, and 102 are facing “sticker shock” where landlords are demanding 20-50% hikes upon renewal.

-

The EMI Advantage: Your home loan interest might fluctuate with the RBI Repo Rate, but your Principal amount is locked.

-

The Math: If your rent is ₹80,000 today and grows at 10% annually, it will be ₹1.28 Lakh in 5 years. If your EMI is ₹1.5 Lakh today, it stays relatively stable, making it “cheaper” than rent within just a few years.

2. “What is the ‘Maintenance GST’ trap in premium societies?”

In many Gurgaon mega-projects (DLF, M3M, Emaar), maintenance is high.

-

The Rule: If your monthly maintenance exceeds ₹7,500, you must pay 18% GST on the entire amount.

-

The Impact: For a 3BHK, if the maintenance is ₹4 per sq. ft. on a 2500 sq. ft. flat, you pay ₹10,000 + ₹1,800 (GST) = ₹11,800/month.

-

Decision Tip: As a buyer, this is a “forever rent” that never ends even after your loan is paid off. Factor this into your long-term EMI outflow.

3. “Is it better to buy near the Dwarka Expressway (DXP) or Sohna Road?”

-

Dwarka Expressway: Prices have nearly doubled since 2022. It is now an “End-User” market. Buy here if you want high capital appreciation, as the Metro extension (expected 2026-27) will likely provide another 15% bump.

-

Sohna Road: Offers better Rental Yields (4-5%) compared to DXP (3%). If you want your tenant to pay off a larger chunk of your EMI, Sohna Road or New Gurgaon (Sectors 82-95) are more mathematically favorable.

4. “Should I consider Fractional Ownership instead of a full EMI?”

In 2026, platforms allow you to invest ₹10-25 Lakh into Grade-A commercial properties (like offices in Cyber City) instead of buying a whole flat.

-

The Benefit: You get 8-10% rental yield (versus 3% in residential) without the headache of an EMI.

-

The Strategy: Many “smart” Gurgaon professionals Rent where they live (to stay mobile) and use their down-payment money for Fractional Ownership to generate passive income that covers 50% of their rent.

5. “What is the ‘Exit Risk’ in Gurgaon right now?”

Gurgaon real estate is illiquid.

-

The Risk: While your “paper value” might grow by 15%, selling a ₹3 Crore+ flat can take 6 to 12 months.

-

The Comparison: If you rent and keep your money in Mutual Funds (averaging 15-18% in the 2024-2026 cycle), you can withdraw your cash in 2 days. Buy only if you don’t need that liquidity for the next 7 years.

Comparison Summary: 2026 Market Pulse

| Scenario | Recommendation |

| New to Gurgaon / Testing a Job | Rent. Prices are at a local high; don’t rush into a peak. |

| Family with kids in local schools | Buy. Avoid the stress of moving every 11 months due to rent hikes. |

| Investor with ₹1 Cr cash | Fractional/Commercial. Residential yields are too low right now. |

| Bachelor/Single Professional | Rent. Maximize your SIPs instead; the market is currently “investor-heavy.” |