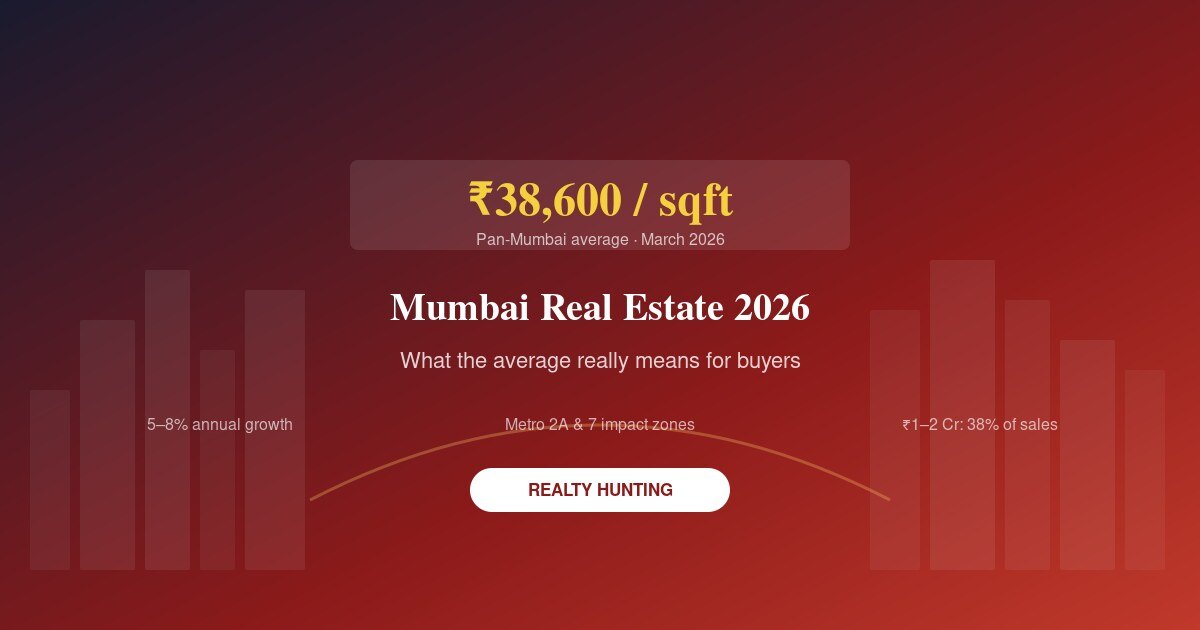

Property Insurance in India 2026: Do You Actually Need It

Key takeaways

- Basic fire insurance for a home starts around ₹1,200-2,500/year for ₹10-20 lakh coverage — genuinely affordable.

- Comprehensive home insurance (fire + theft + natural disaster + liability) runs ₹3,500-5,500/year for the same coverage band.

- IRDAI's standard product, Bharat Griha Raksha, is offered by every general insurer and is the easiest starting point.

- Most Indian homeowners skip this entirely — it's one of the cheapest risk-transfers available relative to what's at stake.

Why this gets skipped so often

Property insurance in India has a strange gap: buyers will happily spend lakhs on home loan processing, interiors, and registration, but stop short of a policy that costs less than a month's maintenance bill. Part of it is awareness — most people simply don't know it's this cheap. Part of it is a belief that "nothing will happen to my flat," which is exactly the thinking insurance exists to protect against.

What property insurance actually costs

| Cover type | Typical coverage | Annual premium |

|---|---|---|

| Basic fire insurance | ₹10-20 lakh (structure only) | ₹1,200-2,500 |

| Comprehensive (fire + theft + natural disaster + liability) | ₹10-20 lakh | ₹3,500-5,500 |

| Bharat Griha Raksha (IRDAI standard product) | Structure and/or contents, fire and allied perils | 0.15-0.40% of sum insured |

For a flat worth ₹80 lakh to ₹1 crore, that works out to roughly ₹12,000-40,000 a year for solid comprehensive coverage — a tiny fraction of what a single fire, flood, or burglary claim would actually cost you out of pocket.

What's actually covered

- Structure cover — the physical building, walls, flooring, fixed fittings.

- Contents cover — furniture, electronics, appliances, jewellery (usually with sub-limits).

- Natural calamities — fire, flood, earthquake, storm, depending on the policy.

- Man-made perils — burglary, theft, riots, in comprehensive plans.

- Liability cover — if someone is injured on your property and sues you, this can cover legal costs.

- Temporary stay expenses — some comprehensive plans cover hotel costs if your home becomes unlivable during repairs.

What raises your premium

Location matters more than most people expect. Homes in seismic Zone IV and V — this includes Delhi and parts of the wider NCR — attract higher premiums than a similar home in a lower-risk zone. Coastal, flood-prone, or cyclone-exposed areas see the same effect. On the flip side, installing CCTV, fire alarms, and basic security systems can bring your premium down, since insurers price in reduced claim likelihood.

Home insurance vs home loan insurance — don't confuse the two

Banks often push a "home loan insurance" or "credit life insurance" product alongside your loan — this pays off your outstanding loan balance if you die or are disabled during the tenure. It is not the same as property insurance, which protects the physical asset itself against fire, theft, and disaster. You genuinely need both to be fully covered, and neither one substitutes for the other. Loan insurance is optional in most cases (despite how banks present it) — property insurance is a separate purchase entirely.

How to actually buy it

- Start with Bharat Griha Raksha — it's IRDAI-mandated, every general insurer must offer it, and it's designed to be simple and comparable across providers.

- Get quotes from 2-3 insurers for the same coverage amount — premiums for identical cover can vary noticeably.

- Declare an honest sum insured — under-declaring to save on premium means you're under-covered exactly when you need the payout most.

- Read the exclusions list before buying, not after a claim gets rejected.

FAQs

Is property insurance mandatory in India?

No, it's not legally mandatory for homeowners, unlike some home loan-linked insurance products banks may push. It's optional but strongly worth having given how cheap it is relative to the risk covered.

What is Bharat Griha Raksha?

An IRDAI-standardized home insurance product that every general insurer in India must offer, covering fire and allied perils on residential dwellings — effective since April 2021.

Does property insurance cover earthquake damage?

Depends on the policy — basic fire policies often exclude earthquake unless specifically added. Comprehensive policies and Bharat Griha Raksha typically include it as a covered peril, but always confirm before buying.

Can renters buy property insurance?

Renters can buy contents-only insurance to cover their own belongings, since the structure itself is the landlord's responsibility to insure.

How is the premium calculated?

Mainly based on sum insured, location/seismic zone, construction type, and security features. Typical range is 0.15-0.40% of sum insured annually for a standard policy.

Bringing it back to your purchase

If you're buying a new home this year — whether in a luxury apartment or anywhere across our live projects — budget for property insurance from day one, not as an afterthought once you've moved in. It's one of the smallest recurring costs in the entire homeownership picture, and one of the most consequential if you skip it and something actually goes wrong. Talk to us when you close a purchase — we can point you toward Bharat Griha Raksha quotes for the exact project and sector you're buying in.