New Tax Rules for Real Estate in 2026 : Impact on Buyers & Developers.

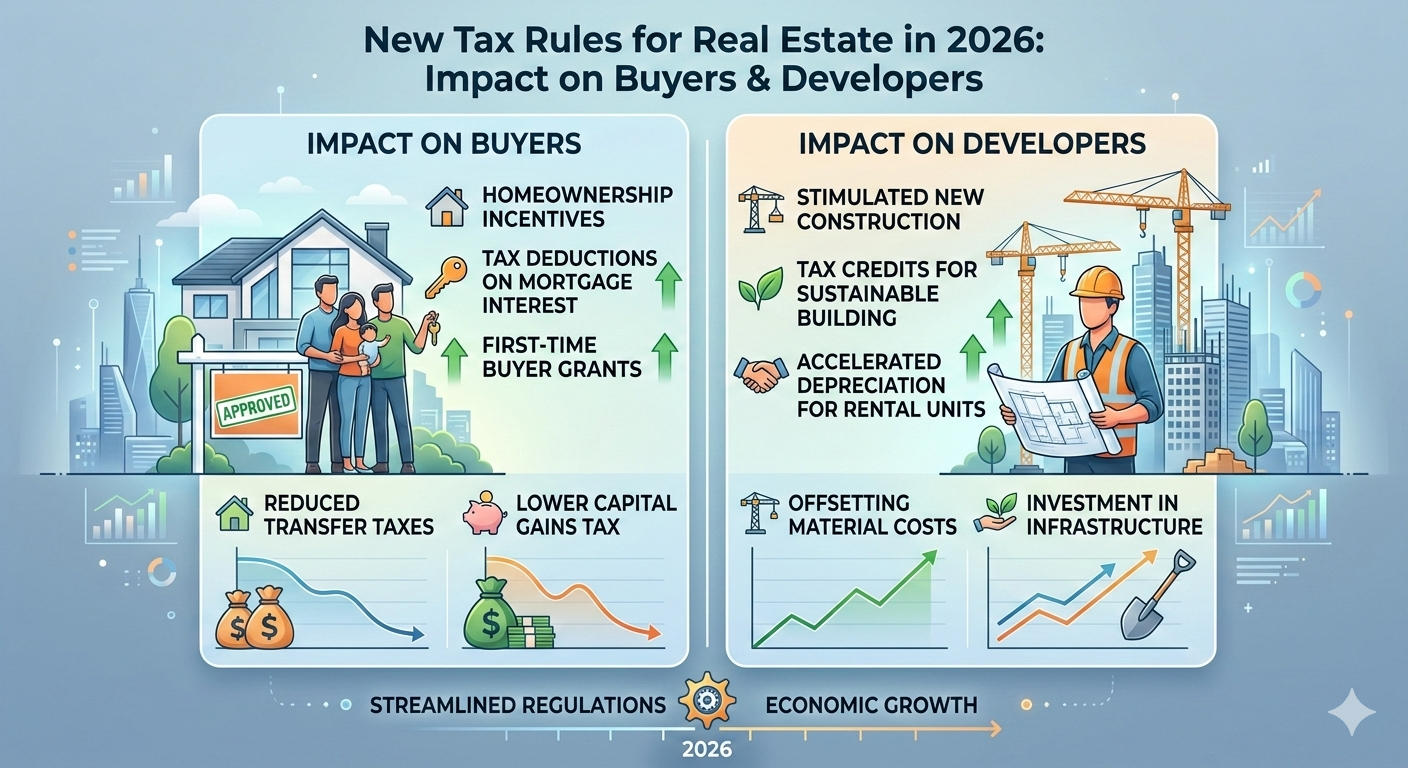

New Tax Rules for Real Estate in 2026 : Impact on Buyers & Developers.: India’s real estate tax landscape in 2026 has moved on from drastic new tax hikes to procedural simplifications and infrastructure-led growth. Even as the Union Budget 2026 has retained several existing structures, it has been the New Income Tax Act and New GST 2.0 rules that have emerged post-Budget as key incentives for buyers and developers.

1. Impact on Homebuyers

The theme for 2026 is “transparency over tax breaks.” While the middle class was expecting an increase in the Section 24(b) interest deduction to ₹5 lakh, this continues to stay capped at ₹2 lakh and the government is promoting New Tax Regime as default.

| Feature | 2026 Rule/Status | Impact on Buyer |

| LTCG Tax Rate | 12.5% (Flat) | Simplified, but no inflation adjustment for new purchases. |

| Indexation Benefit | Removed (for properties bought after July 23, 2024) | Higher tax liability for those selling high-appreciation property. |

| GST on Ready-to-Move | 0% | Continues to be the most tax-efficient way to buy a home. |

| GST Under-Construction | 1% (Affordable) / 5% (Non-Affordable) | Steady pricing; 1% applies if value is < ₹45L and meets area norms. |

| TDS Compliance | PAN-based reporting | No more requirement for a TAN when buying from NRIs; less paperwork. |

Ro-Tip: You are also eligible to buy a second home for rental income, but do keep in mind that GST of 18% is now applicable under the Reverse Charge Mechanism (RCM) if the tenant is a business entity registered under GST, even when it is used for residential purposes.

2. Impact on Developers

GST Rationalization has reduced the cost of key raw materials for developers; however, they face stricter digital compliance in 2026.

Lower Construction Cost – Through GST 2.0 regime, tax on Cement came down from 28% to 18%, Marble / Granite 12% to 5% This has countered some of the inflationary pressure on building costs.

Dedicated REITs for Public Sector land: The 2026 Budget proposed dedicated allocation of REITs for Public Sector. It enables developers to lease out stark lands with the government to create more new “City Economic Regions” (CERs) in Tier-2 and Tier-3 cities.

RCM: Developers are now liable to pay the GST on all supplies (such as sand or labor) made by unregistered vendors. This push towards 100% organized supply chain is “GST 2.0”.

MAT Credit: The Minimum Alternate Tax (MAT) for corporate developers, which was retained at a lower rate of 14%, will end the accrual of any new MAT credits beyond March 31,2026.

Summary Table: Property Classification in 2026

| Property Category | GST Rate | LTCG Rate | Holding Period |

| Affordable Housing | 1% (No ITC) | 12.5% | > 24 Months |

| Luxury/Mid-Segment | 5% (No ITC) | 12.5% | > 24 Months |

| Commercial Property | 12% (With ITC) | 12.5% | > 24 Months |

| Plots/Land | 0% | 12.5% | > 24 Months |

Key Takeaway for 2026

Long-term end-users are benefiting at the expense of “quick-flip” investors in the market. Indexation removal implies you would need to hold on to property longer before meaningful post-tax gains, and the infrastructure focus in Tier-2 cities (as high-speed rail corridors) is where the highest increase in value is likely.

A Big Procedural Change: The PAN Threshold

As of April 1, 2026, the mandatory requirement to quote a Permanent Account Number (PAN) when making property transactions is automatically doubling.

New Limit: PAN is now compulsory only if your transaction amount crosses ₹20 lakh (earlier limit was ₹10 lakh)

Impact: This is a great relief for buyers in Tier-2 and Tier-3 cities and small-value family settlements/gift.

Catch: Experts still suggest quoting your PAN even if your deal is ₹18 lakh. However, a ‘silent’ transaction may still raise automated alerts through triggers set up in the AI systems of the Income Tax Department, which now monitor data obtained through bank credits and registration details if there is ambiguity regarding source of funds.

2. The Long Term Capital Gain “Pick Your Own” Option

For 2027 — the first year a seller will be able to exclude gain on a property they bought through December 31, 2019 in exchange for excluding up to $4 million of gain on another sale that year — would still also be a transition year if the property was purchased before July 23, 2024, offering sellers this special choice:

Lower Rate (12.5%): A flat 12.5% tax on the raw gain (Sale Price – Original Purchase Price)

If held for more than 3 years → Higher Rate + Indexation (20%) – Pay tax @ 20% but adjust purchase price using Cost Inflation Index(CII). The CII is 376 for FY 2025-26.

Strategic note: The 12.5% (no indexation) route is typically cheaper if your property has appreciated slowly. Whereas the 20% (indexed) option is still often the better tax-saving strategy where the property appreciated two or three times over decades.

3. GST 2.0: Maintenance and commercial leasing

In 2026, GST compliance means more than the “purchase price.”

Maintenance Limit: The 18% GST on the maintenance of society is fully applicable. It applies if:

The monthly upkeep costs more than ₹7,500 per member.

The RWA has an annual turnover of over ₹20 lakh.

Commercial ITC Win: Post a landmark Supreme Court ruling, developers can claim Input Tax Credit (ITC) on construction for commercial buildings that are intended to be leased/rented. This has avoided a 12-15% CST “tax on tax” cascading effect that previously made office spaces costlier.

4. NRI Sellers: Simplified TDS

If you are purchasing property from an NRI in 2026, paperwork has been cut down remarkably.

No TAN: Those resident buyers no longer have to apply for a Tax Deduction Account Number (TAN).

PAN Based Challan: You can now pay TDS (Tax Deducted at Source) like any resident Indian, with a simple electronic PAN based challan This eliminates a key friction point for NRIs seeking to liquidate assets.

5. The Incentives of the Circular Economy (For Developers)

Green Construction Tax Breaks in 2026 Budget

Solar & Water: Developers who use certified green materials or integrated water recycling systems are eligible for a 3% rebate on their corporate tax liability, but only within the project during which those sites were utilized.

CPSE-REITS — the government has brought CPSE-REITS, wherein developers can manage/redevelop such enormous land parcels where Public Sector Enterprises are located.

Frequently Asked Questions (FAQs)

For Buyers

Q1: If I purchase a finished flat, is Gst chargeable?

No. If the building is obtained on OC or CC, it will imply a `ready-to-move’ status and no GST will apply. It shall be subject to only Stamp Duty and Registration fees.

Q2: What is the limit on “Affordable Housing” in 2026?

Two criteria needs to be satisfied by a property to be able to avail 1% GST rate:

Cost: The aggregate value of the agreement shall not exceed ₹45 lakh.

Size: Carpet area should be lower than 60 sq. m. in metros (Delhi-NCR, Mumbai, Bengaluru, etc.) or 90 sq. m. in non-metro cities.

Q3: Am I still able to deduct my home loan interest?

* Old Tax Regime: Available, up to ₹2 lakh under Section 24(b).

New Tax Regime (Default): No, this regime does not have the interest deduction for self occupied property.

Q4: Is PAN mandatory for purchasing a small property in a Tier-2 city?

The compulsory threshold limit for quoting a PAN in property transactions is proposed to be raised from ₹10 lakh to ₹20 lakh with effect from 1st April 2026. But experts continue to advise using it to avoid “mismatch notices” from the AI-based tracking measures of Income Tax department.

For Sellers & Investors

Q5: How will Capital Gains Tax be calculated in 2026?

The rules depend on when you purchased the property:

If bought after July 23, 2024: Flat 12.5% LTCG tax you will pay without indexation (inflation adjustment).

Purchase before July 23, 2024: Option for 12.5% without indexation OR 20% with indexation You can choose whichever yields a lower tax bill.

Q6: For how long must I own a property for it to be considered “Long-Term”?

The holding period for real estate, meanwhile, is two years. If you sell before 2 years, the gain is “Short-Term Capital Gains” (STCG) and gets added to your normal income and taxed at your slab rate.

Q7: What are the legal methods to avoid paying Capital Gains Tax?

That was operated under section 54 for reinvestment of the gains in another residential house by within two years (three years if construction). Or, invest up to ₹50 lakh in special bonds (NHAI/REC) within 6 months of the sale under section 54EC.

For Developers

Q8: Should I able to request for Input Tax Credit (ITC) on my projects?

A.* Residential Projects: You do not pay any ITC for residential construction; you bill the lower GST rates (1% or 5%).

Commercial Projects: Yes, on construction materials such as cement and steel for leasing/renting of your space, you can avail ITC.

Q9: Would tax changes have lowered the cost of construction materials?

Yes. The GST was rationalized on Cement from 28% to 18%, Natural Stone/Marble from 12% to 5%. This is anticipated to lower overall project costs by about 3–5%.

Visual Summary: Tax Rates at a Glance

| Category | Rate | Key Condition |

| GST (Residential) | 1% or 5% | Depends on property value (<₹45L). |

| GST (Commercial) | 12% | ITC available for developers. |

| LTCG Tax | 12.5% | Held for >24 months. |

| Stamp Duty | 5%–7% | Varies by state (e.g., Maharashtra vs. Delhi). |

For Buyers & Homeowners

Q1: Has the limit on home loan interest under Section 24(b) been hiked to Rs 5 lakh?

Not yet. Despite a major industry push to raise the limit to ₹ 5 lakh in the Budget for FY26, no such change was made and it still stands at ₹ 2 lakh under the Old Tax Regime for self-occupied properties. This deduction is not available under the New Tax Regime unless property is “let-out” (rented).

Q2: In 2026, can I enjoy tax benefits for Joint Home Loan?

Yes. It is one of the most powerful tax-saving methods out there.

Interest (Sec 24b) : Each co-owner can claim up to ₹2 lakh (Total ₹4 lakh combined for a couple.

Principal (Sec 80C): Each co-owner gets a benefit of up to ₹1.5 lakh (Total ₹3 lakh for a couple)

Condition: Both need to be co-owners on the property and co-borrowers on the loan.

Q3: Is the ₹20 lakh PAN limit only for purchasers?

As per the proposed Draft Income Tax Rules, 2026, the mandatory limit for quoting PAN has been increased to ₹20 lakh — it will be applicable for both buyers and sellers. It also includes Gifts and JDAs (Joint Development Agreements) explicitly. In the case of “Loan Against Property” (LAP), however, banks will not issue a loan without your PAN, irrespective of the transaction value.

For Sellers & Investors

Q4: How does the “Capiatal Gains Account Scheme”(CGAS) work in 2026?

In case you sell a house in FY 2025-26 but do not find one to buy before the tax filing deadline (July 31, 2026), then the gains have to be deposited in CGAS account which is with public sector bank. This essentially “parks” the money and preserves your tax exemption of Section 54 while you search for a house (up to 2 years for purchase or 3 years for construction).

Q5: What does the “12.5% vs. 20%” rule refer to for NRIs?

NRIs disposing of property in 2026 will follow the same option as residents for properties acquired before July 23, 2024:

Example A: 12.5% flat tax on the total gain (No hirer).

Option B: 20% tax with indexation (Inflation adjustment)

Disclaimer: If you are paying through the buyer, deduction of TDS has to be made at payment stage. NB: NRIs should apply for a Lower TDS Certificate ie Form 13 so that the buyer does not deduct tax on the entire sale value, but rather only on the profit made.

Q6: Can I sell one house and buy two to reduce tax?

Yes, as per Section 54 you can bond your capital gains into two residential houses in India, provided your total capital gain does not cross ₹2 crore. This is a once-in-a-lifetime opportunity.

For Commercial Investors and Developers

Q7: What is the “80% Procurement Rule” for developers?

But, to keep the low GST rates (1% or 5%), developers will have to source at least 80% of inputs (cement, steel etc) from GST-registered suppliers. By contrast, if they are buying over 20% from unregistered local vendors, then they themselves will need to pay the tax under what is called the Reverse Charge Mechanism (RCM) at a flat 18%.

Q8: What if I plan to rent an ITC barn as a warehouse?

Yes. Subsequent to clarifications made in recent case laws (ratified in 2026), ITC is available for commercial establishments (office, module, storage) that are meant to be leased or rented. That sharply reduces the effective construction cost for commercial developers relative to residential ones.

2026 Quick-Reference: The “Rule of 2s”

| Metric | 2026 Threshold/Limit |

| Holding Period | 2 Years (24 months) to qualify for LTCG. |

| PAN Requirement | ₹20 Lakh transaction value. |

| Home Loan Interest | ₹2 Lakh (per person, Old Regime). |

| Reinvestment | 2 Houses allowed if gains are under ₹2 Crore. |