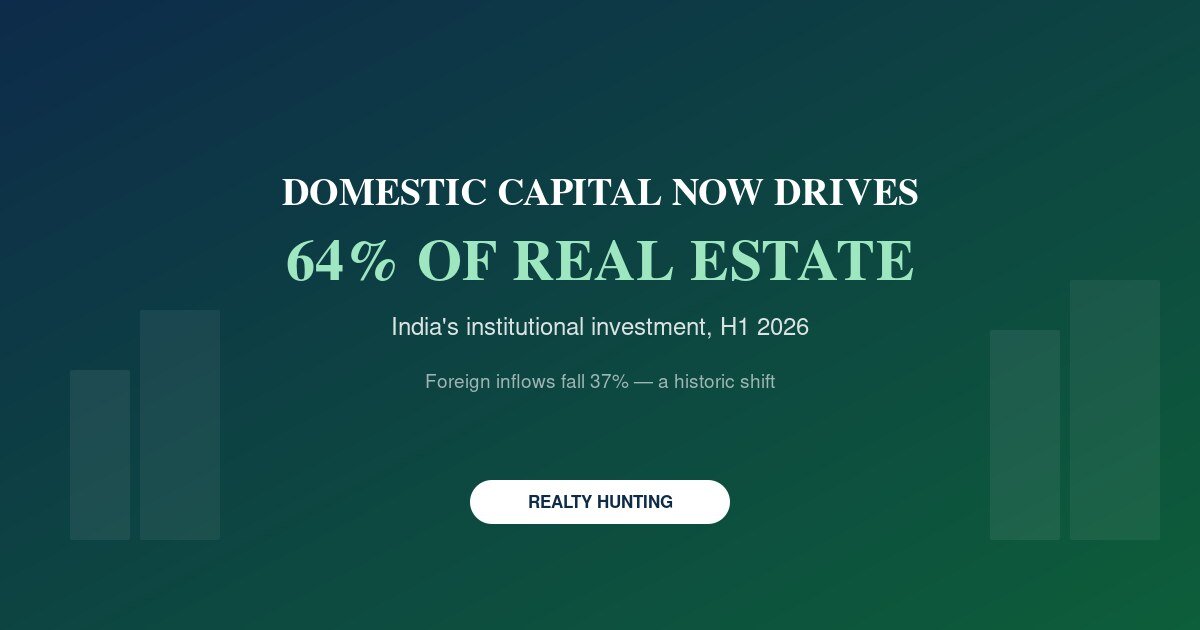

Domestic Investors Now Drive 64% of India's Real Estate Capital — A Historic Shift

For the better part of two decades, foreign capital — global pension funds, sovereign wealth funds and private equity majors — set the pace for institutional real estate investment in India. That's no longer true. In H1 2026, domestic institutional investors accounted for a record 64% share of India's total institutional real estate inflows, while foreign institutional investment actually fell 37% year-on-year. This is a structural shift, not a one-quarter blip, and it changes who's really calling the shots in Indian commercial real estate.

At a Glance

| Metric | Figure |

|---|---|

| H1 2026 total institutional investment | $4.3 billion (up 23% YoY) |

| Domestic capital share, H1 2026 | 64% (record high) |

| Domestic capital growth, H1 2026 | $2.8 billion, +165% YoY |

| Foreign institutional investment change | –37% YoY |

| Q1 2026 domestic share | 76% of $1.6 billion (up 26% YoY) |

| Domestic share trend | 63% (Q3 2025) → 81% (Q4 2025) → 76% (Q1 2026) → 64%+ (H1 2026) |

| Leading sector for capital | Office (54% share, up 34% YoY to $2.3 billion) |

Key Takeaways

- Domestic capital has outpaced foreign inflows for three consecutive quarters, culminating in a record 64% H1 2026 share.

- Domestic institutional investment grew 165% year-on-year to $2.8 billion in H1 2026.

- Foreign institutional inflows fell 37%, hit by global economic uncertainty, inflation concerns and capital repatriation pressures.

- Office real estate remains the biggest magnet for institutional capital, taking a 54% share of total investment.

- This shift gives Indian pension funds, insurers and asset managers more influence over which projects and cities get funded.

What Changed

Three forces explain the shift. First, India's own institutional investor base — pension funds, insurance companies, mutual funds and REITs — has matured significantly, with more capital available to deploy domestically rather than sending it abroad or waiting for foreign co-investment. Second, global macro conditions turned against foreign capital flowing into emerging markets: currency volatility, inflation concerns in developed markets, and pressure on foreign funds to repatriate capital home all reduced the pool of money actively chasing Indian real estate deals. Third, India's listed REIT market has matured to the point where domestic investors have a liquid, regulated vehicle to gain real estate exposure without needing direct foreign-fund partnerships — reducing dependence on foreign capital structures that were once the default route for large commercial deals.

The Office Sector Is Where the Money Is Going

Office real estate reclaimed its position as the top destination for institutional capital, pulling in a 54% share of total investment and rising 34% year-on-year to $2.3 billion. This tracks with what's happening on the ground: GCC (Global Capability Centre) expansion, IT/ITeS leasing, and steady occupancy at listed office REITs like Embassy and Mindspace have kept office assets attractive even in a period when residential luxury housing has grabbed more headlines.

Why Foreign Capital Pulled Back

The 37% drop in foreign institutional investment isn't primarily about India losing its appeal — it's about foreign funds facing pressure at home. Currency concerns, inflationary pressure in the US and Europe, and capital repatriation requirements from limited partners have made global funds more conservative about new emerging-market commitments generally, not just in India. That's an important distinction: this is capital retreating due to conditions in its home markets, not a verdict on Indian real estate fundamentals, which remain solid based on continued leasing and occupancy data.

Who the Domestic Capital Actually Is

"Domestic institutional investors" isn't one homogeneous group — it spans at least four distinct pools of capital, each with different objectives. Insurance companies (LIC and private insurers) typically seek long-duration, stable-yield commercial assets to match their long-term liabilities, making them natural buyers of fully-leased office parks with strong anchor tenants. Pension and provident funds have similarly long horizons but tend to invest through REIT units rather than direct property ownership, for liquidity reasons. Domestic private equity and alternative investment funds (AIFs) are more opportunistic, often targeting under-construction or repositioning opportunities where returns depend on active management rather than passive rent collection. And listed REITs themselves increasingly raise follow-on capital domestically to fund new acquisitions, recycling domestic retail and institutional money back into fresh commercial purchases. Understanding which of these four is behind a specific deal tells you a lot about that deal's risk profile and expected holding period.

What This Means for Developers and Projects

Developers who've historically relied on foreign private equity partnerships for large commercial or mixed-use projects may need to build stronger relationships with domestic institutional players — insurers, pension funds and REIT platforms — as the primary capital source going forward. This could subtly shift which projects get funded: domestic institutions may have different risk appetites, return expectations and city preferences than the foreign funds that previously dominated large-ticket commercial real estate financing in India.

How Different This Is From a Decade Ago

For context on how significant this shift is: through most of the 2010s and into the early 2020s, foreign private equity majors — Blackstone, Brookfield, GIC, CPPIB and similar global funds — were the dominant force behind large Indian commercial real estate deals, often accounting for 60-80% of big-ticket institutional transactions in a given year. Domestic capital's rise to a 64% share in H1 2026 essentially inverts that ratio within roughly a decade. Part of this is India-specific maturation — the 2019 launch of Embassy REIT and subsequent REIT listings gave domestic capital a structured, liquid vehicle that didn't exist before, closing much of the gap that once forced large domestic institutions to co-invest alongside foreign funds rather than lead deals themselves.

Our Honest View

A domestic-capital-led market is generally a healthier, more stable one — it's less exposed to sudden pullouts driven by events entirely outside India's control, like a rate decision in Washington or a currency crisis elsewhere. The risk is concentration: if domestic institutional capital becomes the overwhelming majority source, India's real estate financing becomes more correlated with domestic economic cycles than before, for better or worse. For now, given resilient office leasing and REIT performance, this shift looks like a maturing market rather than a fragile one.

Who Should Care About This

Retail investors considering REITs get an indirect read here — domestic institutions buying into the same office assets that retail REIT investors hold is a vote of confidence in that asset class specifically. Developers planning large commercial projects should factor in that foreign co-investment may be harder to secure than it was two years ago, and domestic institutional relationships now matter more. Anyone tracking macro real estate health should watch whether this domestic share keeps climbing or foreign capital returns once global conditions stabilize.

FAQ

What counts as "institutional" real estate investment? Large-ticket investments by pension funds, insurance companies, sovereign wealth funds, private equity firms and REITs/InvITs — distinct from individual retail buyers purchasing homes or small commercial units.

Why did foreign investment in Indian real estate fall? Primarily due to conditions in foreign funds' home markets — currency volatility, inflation concerns and pressure to repatriate capital — rather than any specific issue with Indian real estate fundamentals.

Which real estate sector is attracting the most institutional money right now? Office real estate, with a 54% share of total institutional investment in H1 2026, up 34% year-on-year to $2.3 billion.

Does this shift affect individual home buyers? Not directly, but it reflects broader confidence in commercial real estate (especially office) that indirectly supports REIT performance — relevant if you hold or are considering REIT units.

Is domestic capital dominance good or bad for the market? Broadly positive for stability, since it reduces exposure to sudden foreign capital pullouts, though a market too concentrated in domestic capital could become more tied to India's own economic cycles.

Which domestic institutions are driving this shift? A mix of insurance companies seeking stable long-term yield, pension funds (mostly through REITs), domestic private equity and AIF funds, and REITs themselves raising follow-on capital — each with different risk appetites and holding periods.

Could foreign investment recover in India's real estate market? Possibly, once global conditions (currency stability, inflation, repatriation pressure) ease — this pullback reflects conditions in foreign funds' home markets more than any structural issue with Indian real estate.

If you want real estate exposure that tracks this institutional trend without buying property directly, read our guide to REITs in India, or explore pre-leased commercial options on Realty Hunting. Get in touch if you'd like a read on how this shift could affect a specific project or city you're tracking.